Virus Tax and Financial Update

Virus Tax and Financial Update (March 17, 2021)

Restaurant Rescue

A $28.6 billion Restaurant Revitalization Fund (RRF) was established by the American Rescue Plan Act of 2021 (ARP), signed into law on March 11, 2021 and designed to provide tax-free federal grants to restaurants, food service and entertainment venues negatively impacted by the COVID-19 pandemic. The grants are calculated by subtracting 2020 gross receipts from 2019 gross receipts to determine the amount of your pandemic-related loss. Reduce that number by the amounts you received in the first and second PPP draws to determine your potential benefit. Once the Fund goes live, the first 21 days will prioritize grant applications from businesses owned and controlled by women, veterans and disadvantaged owners.

Granted funds can be spent on operational expenditures similar to the SBA’s PPP program. Expenses incurred between February 15, 2020 and December 31, 2021 are considered eligible expenditures.

The U. S. Small Business Administration (SBA) is tasked with the administration of this program. The initial $28.6 billion is relatively small and expected to be consumed quickly. Congress has the ability to add funds to the program as needed. It is reported that the SBA will take a few weeks to establish processes and procedures to support the program. SO STAY TUNED TO THIS CHANNEL FOR UPDATES.

May this be your Pot O’ Gold at the end of the St. Patrick’s Day rainbow!

★ Archives ★

Virus Tax and Financial Update (February 26, 2021)

New, “Baby” PPP

In an effort to benefit the smallest of businesses the White House announced earlier this week that starting Wednesday, February 24, 2021 for 2 weeks only businesses with 20 or fewer employees can apply for the Small Business Administration’s (SBA) Paycheck Protection Program (PPP) loans. In addition, the administration changed the formula for calculating the amount of PPP loan available to sole proprietors with no employees. The formula change is probably the biggest news in this announcement. As usual, there is a catch and we’ll discuss that shortly.

The new rule is especially beneficial to sole proprietors. Previously, sole proprietors were eligible for PPP loans based on their 2019 net income (that is, their income less deductible expenses). The new rule increases the amount of PPP loan available to sole proprietors to 2 1/2 months of their 2019 gross income (that is, the amount of their billing or sales without reduction for deductible expenses). When you run this calculation you will realize it is a major change. The SBA announced that the new formula is not allocable to existing PPP loan applications, and there appears to be no way to amend a previously submitted application. If you have not previously applied for the 1st round of PPP loans or the 2nd round of PPP loans then you can benefit by the increased loan available under the new formula.

Here’s the catch. If you did not apply for the initial round of PPP loans and you have from 0 to 20 employees then you are qualified to apply for the newly enhanced PPP loan. However, let’s assume that you applied for the initial round of PPP loans and that your current application is for the 2nd round of PPP loans. One of the requirements of the 2nd round is that you suffered a loss in 2020 of 25% or more of sales in any quarter by comparison to the same quarter in 2019. The change in funding formula announced by the administration in these new PPP loans does not change the requirement that you suffer that measurable business loss from year to year to qualify for your 2nd PPP funding.

Of course, the SBA has not had the opportunity to modify existing applications to achieve the goals of the administration. Bankers are recommending that clients delay their application until the SBA has a chance to adjust to the new rules, but the delay cannot be for too long because the special window for the smallest of businesses is limited to 2 weeks. I urge you to contact your banker right away to determine the process that they intend to take in implementing this new PPP program. Of course as always, the professionals at the Gianno and Freda Financial Center stand ready to answer any questions you might have and provide you with any assistance that you need to help you through these continuing difficult times.

The end of this pandemic seems to be within reach. As we approach a dark anniversary marking the start of this pandemic I urge you all to continue to be kind to one another and never forget to laugh. Better days are ahead.

Now, back to tax season!

Virus Tax and Financial Update (December 29, 2020)

PPPv.2

-or-

Please sir, I want some more

That famous plea from Oliver Twist applies to so many struggling businesses today. The CONSOLIDATED APPROPRIATIONS ACT, 2021 signed by the President provides welcome relief in the form of $284 Billion in funds for a second round of the Paycheck Protection Program (PPPv.2) and relief from the flaws included in PPPv.1. Some of the highlights follow. The SBA has 10 days from the date of enactment (Dec. 27, 2020) to issue rules governing the administration of PPPv.2, and the banks are not ready to take PPPv.2 applications, so we will bring you much more news as it develops.

For PPPv.1 loans:

- The legislation clarifies that the expenses paid for with funds from PPPv.1 ARE DEDUCTIBLE. This reverses the IRS Ruling that said the expenses paid with tax free funds are not deductible.

- Simplified forgiveness rules apply to loans up to $150,000 (as originally anticipated). Loan recipients need only complete a single-page forgiveness application to self-certify compliance with the law. We recommend completing the long-form application first to ensure that your answers are true and correct on the short form. Supporting documentation is not required to be submitted with the forgiveness application but should be kept for a period of 4 years following submission.

- EIDL advances (of up to $10,000) originally reduced the amount of PPP that could be forgiven. The new law clarifies that the EIDL advance will NOT reduce PPP forgiveness.

- Under PPPv.1 if you received a PPP loan you were not allowed to take The Employee Retention Tax Credit against payroll taxes. The new law makes both available. You can recover significant payroll taxes already paid.

For PPPv.2 loans:

The new law allows “second draw” loans for those businesses that qualify for the new PPP. To qualify:

- Your business must have ONE CALENDAR QUARTER in 2020 that had revenue declines of 25% or more compared to the same quarter in 2019.

- You must have used the entire amount of your first PPP loan, or will use such amounts to pay for qualified expenses (NOTE: there is NO requirement that PPPv.1 be forgiven before an application for PPPv.2 can be submitted).

- PPPv.2 only applies to companies with no more than 300 employees, and loans are capped at $2 million per recipient.

- Tax exempt organizations are qualified for the first time, including $15 Billion for live venues, cultural institutions and movie theaters.

Calculating the amount of your PPPv.2 uses a formula of average total monthly payroll costs times 2.5 – except for restaurants and hospitality businesses that get a 3.5 factor. The average total monthly payroll factor can be either for the one-year period prior to the date the loan is made, or calendar year 2019. Again, seasonal employers calculate their maximum loan amount differently. Recipients can choose the length of their covered period (the time to spend PPP funds) but it must be between 8 and 24 weeks. Again, 60% is to be used for payroll, the balance for rent, utilities, interest on prior debt and, newly added, remote work software, personal protective equipment and repairs to damages caused by riots.

Here we go again! Clearly, the SBA has taught us that change is fast and epic. We will keep you posted as this unfolds.

Meanwhile, Happy New Year to us all. If I were a betting man, I would bet that 2021 will be a better year than 2020. Heaven help us. For our part, we can keep smiling. Makes the world a better place.

Virus Tax and Financial Update (November 24, 2020)

IRS Issues Definitive PPP Tax Rulings

But first, a happy and safe Thanksgiving to you and yours…

Last week the IRS released Revenue Rul. 2020-27 and Revenue Proc. 2020-51 providing much-needed guidance on the timing of revenue recognition related to the payroll protection program (PPP) loan forgiveness and the deductibility of the related PPP expenses. These edicts from the IRS further cement their position that while the funds received from the PPP are not taxable income, the expenses paid by the PPP funds are not tax-deductible. In short, the amount that you received from your PPP loan will be treated as a taxable event in the year in which the PPP funds were spent on allowable expenses covered by the PPP. The result of the IRS’s position will substantially increase taxable income in 2020 for many businesses.

Tax planning before the end of 2020 is more critical than ever due to the impact of the taxation of the PPP funds. I urge you to call as soon as possible to do a pro forma projection of your 2020 tax liability and make plans to reduce that tax liability if warranted. More on the IRS proclamations follows.

As we expected, the IRS position states that a taxpayer may not deduct PPP expenses in the year in which the expenses were paid or incurred if, at the end of that taxable year, the taxpayer reasonably expects to receive forgiveness of the PPP loan on the basis of the expenses it paid or accrued during the covered period. The IRS notes that this is the result even if the taxpayer has not submitted an application for forgiveness by the end of the year. What was thought to be a potential strategy to defer the tax into 2021 by delaying the application for forgiveness is a door now closed by the IRS. While some analysts suggest the potential for wiggle room around the term “reasonably expects”, it seems pretty certain that if you spent the PPP funds in accordance with the program strictures you can reasonably expect PPP loan forgiveness. It appears that the only opportunity from relief from the IRS will be legislative action, an unlikely event given the divided government in Washington D.C.

The Rev. Proc. Addresses situations in which the expenses paid for by the PPP are not deducted in 2020 and, for reasons of SBA rejection or taxpayer’s decision not to request loan forgiveness, results in those expenditures qualifying for tax deduction. In that case an amended return can be filed claiming a deduction for those previously not deducted expenditures.

This continues to be a complex area subject to rapid changes requiring you to be vigilant in identifying opportunities to save taxes and keep more of what you earn. Let’s get together sooner rather than later to put a smart tax plan together for you. As we are fond of saying, “it’s not what you earn, it’s what you keep.”

Finally, in this Thanksgiving season let’s remember the apt quote by Gertrude Stein, “Silent gratitude isn’t much use to anyone.” Tell the people you love that you love them.

AND KEEP SMILING!!

Breaking News!!!

Virus Tax and Financial Update (December 21, 2020)

Congress Agrees on New Federal Pandemic Stimulus

A gift from Congress as we celebrate a Merry Christmas, Happy Hanukkah and a festive but safe end of 2020 dominated by the pandemic.

Yesterday D.C. lawmakers agreed in principle to a $900 billion stimulus package intended to stop the U.S. economy from falling off a cliff. The details are still being inked, and we will update you as we learn more, but here’s what we know for now…

Businesses will be allowed to deduct the costs covered by the Payroll Protection Program (PPP) providing a much needed Congressional fix to the IRS position that those costs could not be deducted.

The agreement earmarks $284 billion to revive the PPP. We await details as to who may be eligible for this new round of funding. We are processing forgiveness for the first round of PPP. Let us know if you need help.

Stimulus checks of $600 per person AND per dependent will be issued early in 2021 to those whose income did not exceed $75,000 in 2019.

Federal unemployment benefits for 12 million unemployed are extended for an additional 11 weeks and sweetened by an additional $300 per week (some observers believe this added stimulus will provide a bridge to the vaccine and ease the way for Governors to shut down businesses – we shall see).

The federal moratorium on evictions is extended for another month and is supplemented by rental assistance.

The agreement includes $82 billion for schools and colleges to re-open classrooms safely.

This is a rapidly developing story. The next step is for an actual draft of legislation to pass hours of deliberation in the House Rules Committee, then the consent of all 100 Senators to schedule a vote on the bill. We stand ready to assist you in being vigilant in identifying opportunities to save taxes and keep more of what you earn. Yes, we are fond of saying, “it’s not what you earn, it’s what you keep.”

Finally, in this Holiday Season I turn to the words of Tiny Tim, “God bless us, everyone” Frankly, we need it. Tell the people you love that you love them.

AND KEEP SMILING!!

Virus Tax and Financial Update (October 13, 2020)

Finally, Streamlined (PPP) Loan

Forgiveness Processing!!!

The SBA and the Treasury Department jointly announce the creation of simpler loan forgiveness application, SBA Form 3508S for use by PPP borrowers applying for loan forgiveness on PPP loans with a total loan amount of $50,000 or less. Filing form 3508S also exempts borrowers from any reductions in loan forgiveness amounts based on reductions in full-time equivalent (FTE) employees or reductions in employee salary or wages that would otherwise apply. This simplified loan forgiveness process only applies to approximately 12% of all PPP loans. The primary beneficiaries appear to be businesses that received smaller loan amounts based on profits from their self-employed businesses or their businesses without employees.

Borrowers are still required to submit to the lender documentation verifying payroll costs, eligible business mortgage interest payments, business rental lease payments and business utility payments along with the streamlined application in order to achieve forgiveness. In addition, the borrower is required to verify the eligible payments and accurately calculate the forgiveness amount requested. If your PPP loan amount was less than $50,000 please contact me as soon as possible so that we may commence your forgiveness application.

While the relief is welcome, it leaves too many businesses subject to overly-complex forgiveness procedures. Many business owners and self-employed clients are requesting our assistance in processing the application for forgiveness of their PPP loans. We stand ready to process and file the forgiveness applications at your request.

At this point the vast majority of businesses may benefit by waiting for legislative relief such as that offered by U.S. Senate Bill S. 4117, the “Paycheck Protection Small Business Forgiveness Act”. This bill, which has bipartisan support, provides for automatic forgiveness of a PPP loan that is not more than $150,000 if the recipient submits a one-page form. Approximately 4.2 million of the 5.2 million PPP loans written are for less than $150,000. While this bill relieves a lot of paperwork burden on small businesses, it is not likely to be considered before the upcoming Nov. 3rd elections. Stay tuned.

While the pandemic continues to grip the world you would do well to remember that, “it is what it is” is only half of a great saying. The other half is, “but then, it’s what you make of it”. As always, stay safe, be healthy and make sure you tell the ones you love that you love them.

AND KEEP SMILING!!

Virus Tax and Financial Update (August 18)

When Congress is in session, no American is safe.

-Mark Twain

Here’s what we know today…

On Friday July 31, 2020 members of the United States House of Representatives bolted out of D.C. for their traditional August recess (if you have ever been in D.C. in August, you’d get out of there too!). Problem is, they left without addressing the lapsing of a number of stimulus programs aimed at keeping the economy afloat as the viral pandemic continues. Months ago, the House passed a stimulus package expending nearly $3.5 trillion dollars. The Senate and the Administration proposed alternatives to the House plans. Neither side compromised sufficiently to achieve a solution beneficial to the country’s economy. The impact of the government’s leaders’ failure is yet to be determined. Both sides point the finger of blame.

The leadership has advised members to be prepared for a call back to D.C. to vote if an agreement can be negotiated. An agreement isn’t likely over the next two weeks while the two major parties conduct their quadrennial circuses. Meanwhile, the unemployed receive reduced benefits, businesses continue to suffer from coronavirus related limitations, state and local governments face historic deficits from reduced tax revenues. The SBA has opened the process for forgiving PPP loans, but substantial uncertainty regarding the process (and possible future changes to the process) suggest a wait-and-see approach for now (there is plenty of time to process the forgiveness application).

Strangely, day-to-day life goes on. Summer is winding down (will there be in-classroom schooling or remote learning? What are working parents to do?)

As always, be well, stay safe and most importantly treat each other with kindness.

Your friends at Gianno & Freda

Virus Tax and Financial Update (August 10)

The SBA’s PPP closes, Washington stalemates…

Here’s what we know today…

Saturday, August 8, 2020 saw the passing of the deadline to apply for the Small Business Administration’s (SBA) Payroll Protection program (PPP). On Tuesday, August 4, 2020 the SBA and the U. S. Treasury Dept. issued Frequently asked Questions (FAQs) addressing the process for applying for PPP loan forgiveness. Multiple banks are issuing loan forgiveness instructions to their clients. However, as we have all become accustomed when Washington responds to the pandemic, the path to forgiveness remains unclear. Almost all business advocates are urging Congress to forgive borrowers with loans under $150,000 by self-certifying that they used the loan money in accordance with PPP program strictures. In addition, Washington is under pressure to allow businesses a second loan if their 2020 revenues are between 20% and 50% below their 2019 revenues (depending on different proposals). However, with the House and Senate controlled by opposing parties, and the Administration at odds with Congressional Democrats, producing needed legislation seems improbable, despite the economic pain of the stalemate. While PPP forgiveness applications can commence today, I urge that you do not rush to apply for forgiveness. There continue to be significant unanswered questions, including the definition of utilities, exceptions in the calculations for full-time equivalent employees (FTEs) and questions about methods of documenting expenditures.

Absent Washington providing simple PPP forgiveness, beginning today (August 10) businesses can apply for forgiveness through their lenders. The lender has 60 days to review and approve the application prior to submission to the SBA (believe me, the banks got a commission of 5% of the money lent from the federal government. Since they do not want to keep a loan with a 1% interest rate on their books, they will attempt as much forgiveness as possible). The SBA has 90 days to review the application and can ask for additional information before forgiving all or part of the loan.

There are two SBA forms that can be used to request forgiveness (banks can substitute their own equivalent), SBA Form 3508 and SBA Form 3508EZ.

The Form 3508EZ is close to a check the box self-certifying loan forgiveness application. HOWEVER, it is only available to sole proprietors, independent contractors, and self-employed individuals with no employees. Thus, this form is only available to those with no payroll.

The rest of us (with payroll), are required to use the SBA Form 3508 (which Forbes magazine notes, “would likely require the assistance of a lawyer or CPA.). This is a more complex application requiring extensive payroll calculations and disclosures. Currently, payroll services are offering to produce detailed reports for a fee that can be used to help in the production of the SBA 3508 application.

There are complex rules and examples contained in the FAQs, and we will review those in our next posting.

We will continue to closely monitor this program and other Washington D.C. developments as updates become available. In the meantime, please let us know if we may be of assistance to your specific needs.

Summer is in full swing. Get outside and safely enjoy this beautiful day!

Be well, stay safe and most importantly treat each other with kindness.

Your friends at Gianno & Freda

Virus Tax and Financial Update (June 16)

The SBA’s EIDL Program is Open for Business

Here’s what we know today…

Yesterday the SBA reopened their Economic Injury Disaster Loan (EIDL) Application for qualified small businesses and U.S. agricultural businesses. At this time, they have not announced any changes to the program. So, here is what you can expect:

- Grant of $1,000 per employee employed as of Jan. 31, 2020

- Loan of up to $2 million

- 30-year term

- Fixed interest rate of 3.75%

- No pre-payment penalties

We will continue to closely monitor this program as updates become available. In the meantime, please let us know if we may be of assistance.

Remember to take some time and enjoy this beautiful day!

Be well, stay safe and most importantly treat each other with kindness.

Your friends at Gianno & Freda

Virus Tax and Financial Update (June 4)

PPP House and Senate Reconcile

“Curiouser and curiouser!” Cried Alice (she was so much surprised, that for the moment she quite forgot how to speak good English).”

― Lewis Carroll, Alice’s Adventures in Wonderland

Here’s what we know today…

Last night the U.S. Senate unanimously approved the bill, coined the “Paycheck Protection Flexibility Act”, originally proposed by the House of Representatives on May 28th to modify the terms of the SBA’s PPP Loan. It’s now off to President Trump’s desk for final approval.

But, on to the good stuff! Here’s a breakdown of the changes you can expect to see from the new bill.

- The original 8 week covered period has been extended to 24 weeks. It is important to note that if you are already in possession of PPP funds, this is an election the borrower can make, if you would like, you can forgo the extension and stick with the 8 week covered period. More details to come on how you would go about making this election. New PPP borrowers will automatically have a 24 week period, not to extend beyond December 31, 2020.

- The 75/25 rule has been replaced with a more favorable 60/40 expense split. The new bill states 60% of PPP funds MUST be used on payroll expenses- here’s the BIG difference- if you do not spend 60% on payroll, your entire loan will not be forgiven! This is a notable difference from the prior version of the bill where the borrower was only required to reduce the eligible amount of forgiveness if they fell short of the 75%. The remaining 40% of PPP funds can be used on other covered expenses (i.e. rent, utilities, mortgage interest).

- The June 30 deadline to restore your workforce and wages to pre-pandemic levels has been extended to December 31, 2020.

- If you had employees who turned down your offer to return to work, then subsequently were unable to hire replacements in an effort to return your workforce to February 15, 2020 levels, the new bill allows an adjustment for these individuals in your forgiveness calculation.

- The term of the PPP loan has been extended from 2 years to 5 years. Borrowers already in possession of PPP funds will need to make an election for the 5 year term, this will need to be coordinated with and approved by your bank. The interest rate on the loan will remain at 1%.

- Previously, borrowers in possession of PPP funds were not allowed to delay payment of payroll taxes, the new bill states that you can now delay these payments if you so choose.

We will continue to closely monitor these new developments as they become available. In the meantime, get outside and enjoy this beautiful day!

Be well, stay safe and most importantly, treat each other with kindness.

Your friends at Gianno & Freda

Virus Tax and Financial Update May 28

Greetings to you and yours. Best wishes for your continued health and safety as governments commence easing COVID-19 restrictions. The lifting of restrictions reminds me of the Wizard of Oz scene where the good witch Glinda sings to the Munchkins,

and meet the young lady who fell from a star.

As we poke our heads out from under the blankets, the news today focuses on the two prominent Small Business Administration (SBA) disaster aid programs, the Payroll Protection Act (PPP) and the Economic Injury Disaster Loan (EIDL) Program. First, the EIDL, then, the more complex PPP and its forgiveness provisions.

Here’s what we know today…

STIMULUS PAYMENT UPDATE

The U.S. Treasury is now issuing PREPAID DEBIT CARDS for some of the stimulus payments (how unusual). The card will arrive in a plain envelope from “Money Network Cardholder Services” (talk about suspicious!). It’s ok, it’s safe, it really is a debit card. You must call to set up a PIN, but then should be able to use it as any other debit card. More at EIPcard.com.

EIDL

The phone’s been ringing here at Gianno and Freda with clients reporting the receipt of their EIDL loans from the SBA. Remember some months ago when the SBA deposited a $1000 per employee grant into your bank account? Well, that was only the first round of the EIDL. After a long and mighty silence the second round of the EIDL is underway.

In this round, you receive an email from the SBA reporting the result of your loan application submitted a long time ago. Typically, the SBA email advises you of the award of a loan generally between $50,000 and $150,000. It asks you to follow a link online to verify your acceptance of the loan amount (or a lesser amount if you choose), confirm your bank, and provide answers to personal questions allowing the SBA to confirm that you are the authorized recipient.

About 5 days after you reply to this email you will receive another email requesting that you electronically sign the attached SBA loan documents. A day or two after you sign and submit the documents the funds magically appear in your bank account. Later, an SBA attorney will call you to ask you to sign hard copies of the loan documents and mail them to the SBA.

The loan terms are quite favorable. These are 30 year loans with a fixed 3.75% rate of interest. No payments are required for the first year. The monthly payment on a $150,000 loan approximates $700 (or, as Gianno and Freda’s fave Jeff L. smilingly notes “that’s a car payment!”). I consider the loan a cash cushion against the uncertainty of the pandemic. It may be beneficial to hold it for a while to ensure the return of relatively normal commerce levels. Since there is no prepayment penalty you can return some or all of it on your schedule. Give me a call to discuss the rules regarding the acceptable uses of these funds.

PPP – The loan forgiveness phase

On Friday May 15, the SBA released the application for the forgiveness of PPP loans, and we have been following rapidly changing developments in the rules to achieve forgiveness.

The forgiveness application specifies that all PPP funds must be spent within 8 weeks of receipt of the monies in order to achieve loan forgiveness. However, separate pieces of legislation are under consideration in both the House and the Senate that will extend the time to spend the funds for businesses closed by state governments and redress the balance between payroll (75%) and non-payroll (25%) expenditures that will qualify for forgiveness. Additionally, legislative proposals seek to extend the payback period for the unforgiven PPP monies to more than the existing 2 year maturity.

The uncertainty caused by the legislative process comes in the face of the update to the forgiveness rules late last week AND as the first of the PPP recipients are a week away from completing the 8 week period specified in the original legislation. A planning nightmare.

The complexity of the forgiveness calculation is staggering. The application and instructions are 12 pages long. Calculated amounts carry across multiple subschedules. In the coming week I will attempt to guide you through the maze of requirements. Suffice it to say that the calculations clearly require you to satisfy BOTH the dollar amounts and employee headcount to achieve full forgiveness.

AS ALWAYS, UPDATES WILL FOLLOW

AS NEWS DEVELOPS.

Your friends at the Gianno and Freda Financial Center

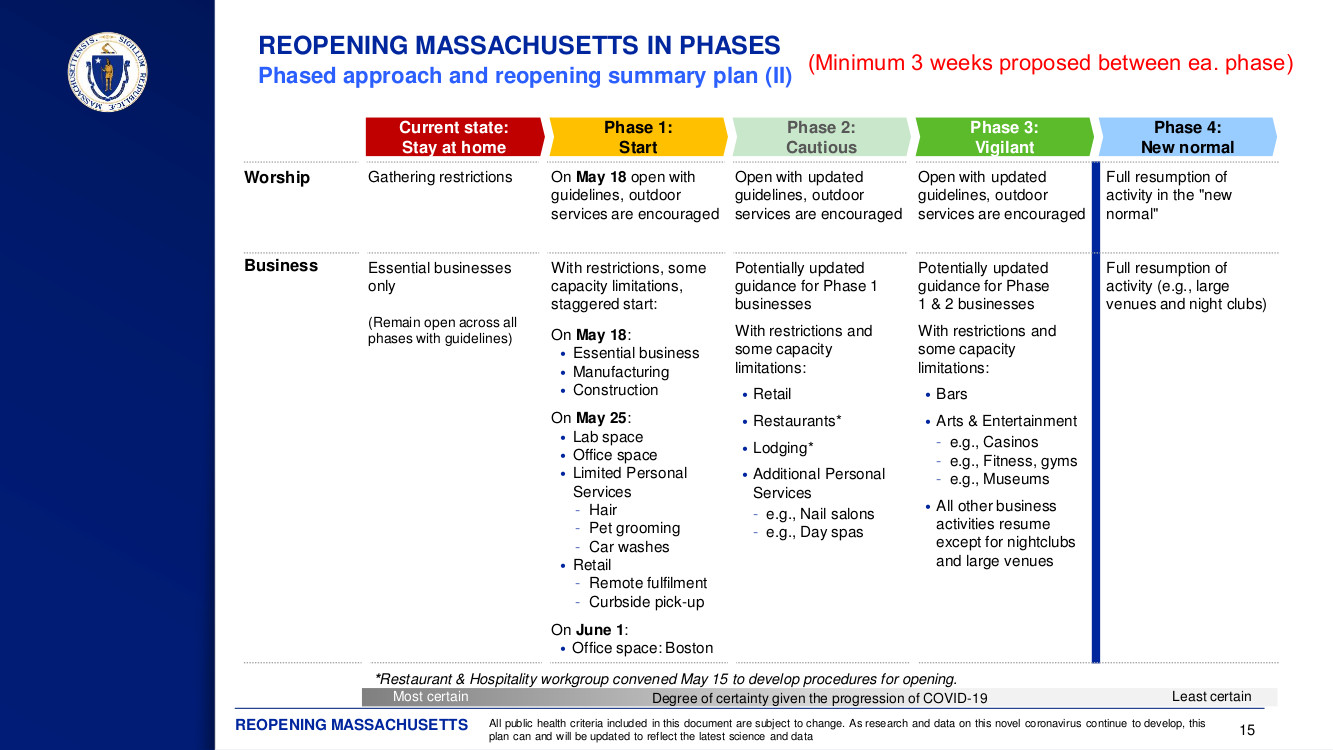

Download Chart as a PDF here: MA-Reopening-4-Phases

THIS TIME, NO NEWS IS NOT GOOD NEWS

Virus Tax and Financial Update May 15

If you hold PPP monies, and your business is closed by the government due to this pandemic, you have until Monday, May 18, 2020 to give the PPP money back and qualify for the LIKELY more beneficial Economic Recovery Credit (ERC) program. Read on….

Recall yesterday that our world was abuzz with rumors that a major announcement was coming TODAY from the SBA that would benefit holders of PPP monies. At least one banker was telling clients that the time to use PPP funds was to be extended from 8 weeks to 12 weeks.

Well, here we are, it’s TODAY, it’s 3:30 p.m., and the big news is….

PPP loans for under $2 million are unlikely to be audited regarding the certification that the funds were needed to support the business. Excuse me but, this blockbuster leaves me yawning.

All the worry is over certifying the following statement to obtain PPP funds,

“all borrowers must certify in good faith that [c]urrent economic uncertainty makes this loan request necessary to support the ongoing operations of the Applicant.”

Are you kidding me? There is not a single closely-held business in my experience that would have trouble answering that in the affirmative – none of us know what economic stresses we will face over the coming years.

UPDATES WILL FOLLOW AS NEWS DEVELOPS.

safely and be kind to one another

Keep smiling, and don’t forget to laugh!!

Your friends at the Gianno and Freda Financial Center

FLASH NEWS – TIME SENSITIVE – LAST MINUTE CHANGE

Virus Tax and Financial Update May 12 – Two Days Later!

Incredible – just incredible! Two days ago, I notified you of the looming May 14 deadline to return PPP monies in order to qualify for the ERC.

While I published that warning based on the available information….

THE SBA YESTERDAY EXTENDED THE MAY 14 DEADLINE TO MONDAY MAY 18

Thus, you now have until Monday to decide if you want to give back the PPP money to qualify for the ERC. Further, there are rumors that the SBA will announce tomorrow that is FINALLY considering extending the period for spending PPP monies beyond the 8 weeks.

But, these are only rumors based on the intense pressure the SBA is feeling from business and professional interest groups.

YOU MUST STAY TUNED TO THIS CHANNEL. UPDATES WILL FOLLOW AS NEWS DEVELOPS.

This continues to be an issue faced by all businesses that are closed by their state governments and holding Payroll Protection Program (PPP) funds they may have received up to 3 WEEKS AGO. There is an alternative program, the Employee Retention Credit (ERC) that might have more benefit for you. In a nutshell, the ERC provides a 50% tax credit for up to $10,000 of payroll paid per employee for wages paid after March 12, 2020 and before December 31, 2020. YOU CANNOT PARTICIPATE IN BOTH THE PPP AND THE ERC – YOU MUST CHOOSE!

Most importantly, be healthy, conduct yourself safely and be kind to one another.

On a beautiful day it is hard to remember we are in a pandemic – get outside, enjoy and be safe. Thanks!

Your friends at the Gianno and Freda Financial Center

URGENT – TIME SENSITIVE – PPP or ERC what’s better for me?

Virus Tax and Financial Update Part 1 (May 12)

The urgency comes from the May 14 decision deadline faced by all businesses that are closed by their state governments and holding Payroll Protection Program (PPP) funds they may have received up to 3 WEEKS AGO. There is an alternative program, the Employee Retention Credit (ERC) that might have more benefit for you. In a nutshell, the ERC provides a 50% tax credit for up to $10,000 of payroll paid per employee for wages paid after March 12, 2020 and before December 31, 2020. YOU CANNOT PARTICIPATE IN BOTH THE PPP AND THE ERC – YOU MUST CHOOSE. Details and an example follow. Much else happened over the weekend. Other developments are addressed in today’s PART 2 email. This urgent email is focused exclusively on businesses closed by the state and holding PPP funds.

Here’s what we know today-

FACT: Your bank has funded your PPP loan.

FACT: The Small Business Administration (SBA) mandates that you have 8 weeks from the date your bank gave you the money to spend these funds, no less than 75% of the expenditures in payroll, no more than 25% in rent, utilities and interest on pre-existing loans. Any funds that you spend in this way are eligible for forgiveness under application to the SBA. Any funds not spent under this formula are subject to repayment within 2 years.

FACT: PPP monies are not taxable, but, in an IRS ruling last week, the expenses these funds pay are NOT deductible. It is a zero sum for income tax purposes.

FACT: the SBA Economic Injury Disaster Loans (EIDL) are beginning to fund and will continue to fund over the next few weeks. The loans are typically for $150,000 and carry a 3.75% interest rate with a 30 year amortization, without pre-payment penalties. See today’s Part 2 email for more details.

ASSUMPTION: Your business is closed under orders of your state government, and you have been holding these funds for one, two, or three weeks.

PROBLEM: If you cannot spend the PPP funds in 8 weeks from funding (as required above) you will owe these monies back in 2 years.

The difficulty in analyzing this decision lies in the shortage of reliable information. For example, there is great pressure on the SBA to modify the beginning of the 8 week spending period to coincide with the date the state government allows businesses to re-open. Despite this pressure, the SBA remains silent, leaving the reasonable conclusion that the SBA will not change. Thus, if your state has your business closed for another week, or two, or three, you are left with precious little time to effectively spend the PPP funds to achieve the desired loan forgiveness.

EXAMPLE

Steve has a restaurant business that is closed by the state. Three weeks ago he received $70,000 in PPP monies to help him fund his payroll and keep his employees working. However, the state has his business closed at least until May 18. This gives Steve 4 weeks (or less if the state extends the business shutdown) to spend what was calculated to be 2 ½ months average 2019 payroll. It is highly unlikely that Steve will spend even half of the $70,000 of PPP monies, and needs to pay back the balance (within 2 years, less if Steve decides to prepay without penalty).

In 2019 Steve’s business had 15 employees that were paid $10,000 or more. Let’s assume that, because of the pandemic, for 2020 he only has 12 employees that make $10,000 or more between March 12 and December 31 2020. That’s $120,000 of payroll (12 employees times $10,000). Under the ERC, Steve’s business earns $60,000 in refundable income tax credits.

That is, $60,000 in taxes that are offset by the credit, and, if the businesses total taxes are less than $60,000, the excess credit is paid to Steve’s business (actually, flow through to Steve if he is an S corporation) (tax credits are MUCH preferred to tax deductions, and often more beneficial than tax-free income).

So, if the SBA does not move the start date for the PPP, Steve needs to decide, do I need the cash so desperately that I will take the chance that I might only get $25,000 or $30,000 of PPP monies forgiven, OR, am I better off giving the PPP monies back and taking the chance that business will bounce back enough to potentially provide a $60,000 tax credit?

This is a case by case analysis that results in an irrevocable decision that must be decided quickly and with limited information. Give us a call to discuss how his choice may apply to you and your business.

We will update as news warrants – always happy to address your specific questions.

Virus Tax and Financial Update Part 2

URGENT – TIME SENSITIVE – May 13 deadline to provide IRS with

bank information to direct deposit stimulus payment

-and-

Here come the EIDL loans!!!

Here’s what we know today-

You have until tomorrow, May 13, 2020, to provide the IRS with your bank information to expedite the deposit of your stimulus check. A couple of weeks ago I reported IRS planned to establish a web based portal for you to add your banking information for a speedier direct deposit. As reported last week, the IRS successfully launched that portal. Now when you go to IRS.gov and click on “Get My Payment”, and provide answers to their security questions, the site will direct you to a location where you can enter your banking information. The resulting direct deposit method can save you months of waiting for your stimulus check.

Well now, here come the EIDL loans… The SBA is notifying applicants that their SBA EIDL loan applications are in process and will fund soon. If your loan application number begins with the number 3, know that you are underway. Theloans are typically for $150,000 and carry a 3.75% interest rate with a 30 year amortization, without pre-payment penalties. These funds should be used to continue the normal operations of your business. Contact us for further details on which expenditures would be considered eligible.

We will update as news warrants – always happy to address your specific questions.

Most importantly, be healthy, conduct yourself safely and be kind to one another

On a beautiful day it is hard to remember we are in a pandemic – get outside, enjoy and be safe. Thanks!

Your friends at the Gianno and Freda Financial Center

Virus Tax and Financial Update (May Day!)

In a nutshell, we are receiving our Stimulus checks, the first round of the SBA’s PPP loans are funded, and the second round is moving right along. Nobody has heard a peep about the SBA’s EIDL loans that we all applied for a month or more ago. Let’s look at each of these three programs in more detail…

Here’s what we know today-

Stimulus checks are being direct deposited… a couple of weeks ago I reported IRS plans to establish a web based portal for you to add your banking information for a speedier direct deposit. As reported to me last Friday by favorite Chatham attorney Paul L., the IRS has successfully launched that portal. Now when you go to IRS.gov and click on “Get My Payment”, and provide answers to their security questions, the site will direct you to a location where you can enter your banking information. The resulting direct deposit method can save you months of waiting for your stimulus check. Thanks Paul!

Thanks for the Payroll Protection Program (PPP) check – now what am I supposed to do with it? Late last week Congress authorized $320 billion of new funding for the second round of the PPP. Second round applications were reported to be double the number of the first round applications (so many that they crashed the SBA’s E – Tran processing system). It is expected that round two will run out of funds in less time than it took for the first round to break the bank. Now that round one is funded and round two will be funded over the next two weeks, loan recipients anxiously inquire about the rules governing these funds. I have the answers. I will give you the framework of the general rules herein but urge you to call me to discuss issues and concerns specific to you and your business. Despite these rules, major unanswered questions continue to cause concern.

The SBA has issued an interim final rule governing the PPP. That rule, in section r., specifies that the proceeds of a PPP loan are to be used for:

i. payroll costs

ii. costs related to the continuation of group health care benefits during periods of paid sick, medical, or family leave, and insurance premiums

iii. mortgage interest payments (but not mortgage prepayments or principal payments)

iv. rent payments

v. utility payments

vi. interest payments on any other debt obligations that were incurred on or before February 15, 2020.

The rule further specifies that at least 75% of the PPP loan proceeds shall be used for payroll costs (by calculation then, 25% or less on the other allowed expense categories). If, during the eight week period beginning on the date you receive your loan proceeds, you maintain payroll levels, both in terms of dollar amounts and headcount, at the average 2019 levels that you disclosed on your PPP loan application, you can apply through your bank for forgiveness of the entire loan. Failure to spend 100% of the loan in accordance with the rules will still qualify you for partial loan forgiveness on a somewhat proportional basis.

The rules contained in ii. through vi. appear relatively straightforward. Not so clear is how to satisfy i. payroll costs. The rule specifies that you are attempting to achieve both a dollar amount and headcount in order to qualify for loan forgiveness. Thus, the business owner that says, “My business is closed. What if I just write myself out a payroll check for the full amount of the loan?” is neglecting to consider the headcount aspect of the forgiveness and will likely fail to achieve most, if not all, of the forgiveness feature. However, the rule does not specify who must be hired, nor the level of pay that must be provided to employees or the business owners (should I give myself a raise? – PROBABLY!). This lack of direction from the SBA is frustrating, but possibly provides opportunities to maximize your benefit from the PPP loan funds.

STILL UNANSWERED… how can a business maintain 8 weeks of payroll activity at 2019 levels when the state government has shut down all but essential businesses until at least May 18? The SBA maintains its maddening silence on this issue. It appears that the SBA will maintain its eight weeks from funding position despite pressure from loan recipients to move the eight week period out to a beginning date equal to the date that the state governor allows businesses to reopen. This new interim final rule is still open to public commentary and yours truly is crafting a commentary that specifically addresses this issue. Let’s hope that reason prevails in this matter.

The interim final rules, in section s. specify that “if you use PPP funds for unauthorized purposes, SBA will direct you to repay those amounts. If you knowingly use the funds for unauthorized purposes, you’ll be subject to additional liability such as charges for fraud.” This language clearly limits any attempts to use the funds for purposes other than those specified in the PPP legislation. Clearly, this is a complex area and I’m happy to provide whatever guidance I can to you. Call me.

Oh, and one more thing about the PPP. The IRS has ruled that expenses paid with PPP money are not deductible expenses (because the PPP funds are not taxable). For those in a 25% combined state and federal income tax bracket this is a significant reduction in the benefit of the PPP funds. If the purpose of the funds is to stimulate business activity, why damper it with the tax burden?

The Economic Injury Disaster Loan (EIDL) program originally promised $10,000 grant checks to applicants within 3 days of applying for a loan of up to $2,000,000. Few received the promised grant checks, and the vast majority of those were for significantly less than $10,000. But the larger question is this, where are the loans? Applications in some cases were submitted almost 2 months ago and we haven’t heard a word about the amount of loan available to you nor the term of the loan (which is promised to be up to 30 years at the SBA’s discretion).

Hello? – SBA, is anybody home?

We will update as news warrants – always happy to address your specific questions.

Most importantly, be healthy, conduct yourself

safely and be kind to one another

On a beautiful day it is hard to remember we are in a pandemic – get outside, enjoy and be safe. Thanks!

Your friends at the Gianno and Freda Financial Center

Virus Tax and Financial Update (April 23, 2020)

The five week total of job losses increases to more than 26 million, at least nine times the worst weekly rate of job decline in the Great Recession of 2008 – 2009. The $349 billion of first round funding of the Small Business Administration’s (SBA) Paycheck Protection Program (PPP) ran out in two weeks. According to the Treasury Secretary and the U.S. SBA Administrator, “the SBA has processed more than 14 years’ worth of loans in less than 14 days.” Larger banks such as Wells Fargo, Bank of America, JP Morgan Chase and U.S. Bank have been sued for favoring some applicants over others, and for other charges of mismanagement of the program. Amidst much criticism of the banking community in administering the SBA program, smaller banks and community-based banks were most effective in obtaining PPP funds for their customers.

Congress has agreed in principle to round two of PPP funding. Final House approval may be achieved as early as today. Since small businesses account for over 99% of U.S. businesses and nearly half of the nation’s workforce, the stakes in round two are significant. Further, it is likely that there will not be a round three of funding. It is important to get this right. We can help you with any of your application needs.

Here’s what we know today –

PPP round two will be funded with $310 billion of federal funds. It is anticipated that this round may run out of money in less than half the time of the first round. The program, administered by the SBA in conjunction with banks, is designed to provide small businesses with loans equal to 2.5 times their monthly payroll costs. Once funded, the business must use the funds over an eight week period to maintain payroll amounts and headcounts equal to the average payroll of 2019 in order to apply for forgiveness of the loan (businesses are directed to spend 75% or more on payroll costs, but can also use 25% or less on rent and utility costs). The SBA has given precious little direction as to how businesses can satisfy the requirements to successfully apply for loan forgiveness. We are monitoring this issue closely and will keep you posted as news becomes available.

Where’s my Economic Injury Disaster Loan (EIDL)? The SBA has been remarkably silent regarding the program that originally promised $10,000 checks to applicants within 3 days of applying for a loan of up to $2,000,000, and no new applications are being accepted. Some applicants received notice from the SBA that their initial $10,000 grant was reduced to $1000 per employee who was on the payroll on January 31, 2020. Others have heard nothing from the SBA. Nor has there been any indication of amounts to be loaned under this program and when those loans will be made available. The silence following the announcement of this program has been astounding.

Stimulus Payments started depositing last week. If the IRS has your banking information on file you may already have received your payment. If they do not have your banking information on file they may eventually get that information through the Social Security Administration if you are on Social Security. Many individuals go to the IRS website to inquire as to the whereabouts of their stimulus payment only to find that the IRS is unable to provide them any information. I generally find there to be no explanation in these cases and you may simply be in the queue waiting for a paper check (that the IRS says can take up to 20 weeks).

We are constantly monitoring news and government announcements for information beneficial to you. I urge you to contact us with any questions or concerns (of any nature!).

Thank you for choosing the Gianno and Freda Financial Center to be your trusted advisor in these trying times. We are happy to be of service to you.

Spring is in the air – get outside and enjoy!

Your friends at the Gianno and Freda Financial Center

Palm Sunday, April 5, 2020

There have been a number of developments this weekend regarding the two main loan programs being administered by the United States Small Business Administration (SBA). The two programs are the Economic Injury Disaster Loan (EIDL) and the Paycheck Protection Program (PPP). To review, the EIDL is applied for directly through the SBA at its website. The PPP is applied for through your local bank (however, some local banks are not taking SBA PPP loan applications). We are preparing applications for both loan programs for any of you that request our assistance.

The CARE Act was signed into law just a week ago Friday. It included a provision for $349 billion dollars in loans to support the PPP. The SBA was charged with administering this program. The Treasury and the SBA announced the first day for accepting PPP loan applications was Friday, April 3.

There is a wide disparity in the performance of the banks in accepting loan applications. The Treasury Department announced that on Friday $1.8 billion of PPP loans were processed, almost exclusively from Community Banks. Bank of America reports that they processed over $6 billion in PPP loans on Friday. Most large banks appear to be hamstrung in their ability to administer their roles in this critically important benefit for small businesses. Some banks say they are not currently taking applications. Other banks say that they’re taking applications only from existing customers (this despite the fact that the SBA has announced that business owners can apply to any participating SBA lender). Each bank has differing documentation requirements. Business owners are getting little direction from the banking community.

It is our experience that some banks are working effectively to receive and process PPP applications. Give us a call to determine which banks might be best suited to serve your needs. We recommend that you immediately submit an application for the PPP loan program. The SBA expects this program to be oversubscribed, and funds may run out within a few weeks. Do not delay.

The SBA significantly streamlined the application for the EIDL on their website over the past week. The application can be completed in as little as a half an hour. A critical question in the initial application process asks if you would like in EIDL advance of up to $10,000. The answer to that question is YES. According to the SBA website this advance will provide economic relief to businesses that are currently experiencing a temporary loss of revenue. Funds will be made available following a successful application. This loan advance will not have to be repaid.

Businesses can borrow up to $2 million through the EIDL. The interest rate is 3.75% and loan terms can be up to 30 years at the discretion of the SBA (although most terms will be shorter). Significantly, the SBA will not charge a prepayment penalty for these loans. This gives a business considerable discretion as to when they can return funds to the SBA.

It is my belief that both of these programs can significantly benefit small businesses in these concerning times. I urge you to ensure that you complete your applications as soon as possible. Please let us know if we can be of help to you in this important matter.

Be healthy, conduct yourself safely, and most importantly, be kind

March 27, 2020 Truly hoping this finds you continuing safe and healthy practices.

Today’s Covid-19 tax and financial news update

Massachusetts Tax Deadline Moved

Massachusetts FINALLY comes to its senses and mirrors the Federal extended 2019 income tax filing deadline of July 15, 2020. The Commonwealth had delayed adopting the Federal deadline because of the absolute crushing the state budget is getting with the loss of business revenues during the shutdown. The Federal government may need to provide support to the states in this critical time.

Coronavirus Stimulus Payments from the federal government

There is no application required for the much vaunted $1200 per person stimulus checks coming from the IRS. These checks will be direct deposited if the IRS has your direct deposit information from prior tax filings. If they do not, they can mail a check to your “last known address”. The IRS has 15 days to notify you of the method and amount of payment. Notify the IRS if you’ve moved recently.

The amount of the check is income dependent, with individuals with adjusted gross income above $99,000 and couples above $198,000 receiving no check. The income calculation is based on 2019 income if your return is filed, 2018 if the 2019 is not yet filed.

Markets

Worldwide markets continue to roil in the face of the pandemic. Major directional shifts occur with every change in the news. Clearly, Mr. Market is in charge. For the uninitiated, Mr. Market (first introduced to us by Benjamin Graham, the legendary investor and author) is a hypothetical investor who is driven by panic, euphoria, and apathy (on any given day), and approaches his investing as a reaction to his mood, rather than through fundamental (or technical) analysis. We continue to maintain a long term view of your finances. The plans that we implement for you worked before the current troubles, and will continue to support you as we move ahead.

I urge you to call me for direction with any of your concerns in this troubling time. Together, we will arrive at quieter shores.

Stay safe. Be healthy. Tell the ones you love that you love them today.